As independent financial advisers based in Manchester, we use cashflow modelling to help clients understand what their future could look like financially.

It’s not always easy to picture what the future looks like financially. Cashflow modelling takes the guesswork away by showing you, using historical market data, how your money could perform over time across a range of back-tested scenarios.

We map out your income, contributions, spending, assets and investments to build a forecast you can rely on. This allows you to test different scenarios, such as retiring earlier, phasing into retirement by going part-time, buying a second home or helping your loved ones, so you can see the long-term impact of your decisions before you make them.

Cashflow modelling is one of the most effective ways to understand how much you need to retire in the UK and when you can realistically afford to stop working.

For many clients, it’s the first time they’ve had a clear answer to whether they can retire, what that actually looks like financially, and the confidence to act on it.

What is cashflow modelling and why does it matter?

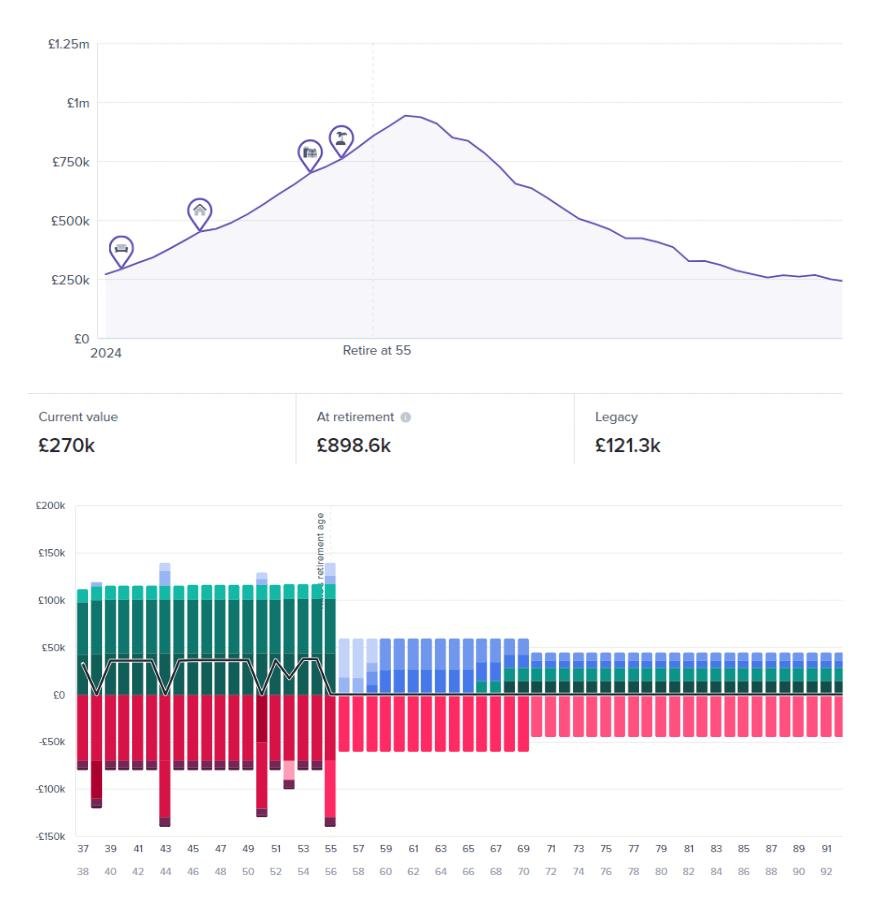

Cashflow modelling brings your finances to life by pulling your pensions, investments and savings into one clear plan, showing how it could play out over time using real historical market data. This helps you understand how robust your plan is across a range of scenarios — not just one outcome.

For most people, the biggest uncertainty isn’t how much they have, it’s whether it’s enough. Cashflow modelling gives you that clarity, so you can make informed decisions with confidence.

Understanding Your Position

We start by building a full picture of your finances, including your income, spending, pensions, investments, property and future plans, along with what you’re currently contributing to those plans and where they’re invested.

Building Your Plan

We map everything into the financial forecast including investment growth, inflation, personal tax and any product-level tax, alongside your future goals and one-off events. This gives you a realistic and joined-up view of your financial future.

Testing Different Scenarios

We test your plan across a wide range of historical scenarios to understand how sustainable it is over time. This allows us to see whether your plan is likely to last, how it performs in different market conditions, where risks may lie and what changes could improve it. It’s not about predicting the future, it’s about understanding how resilient your plan is.

Turning It Into Action

We use the forecast to guide real decisions, such as how much to contribute to pensions, how and when to take retirement income and how your investments should be structured. This often leads into wider planning and implementation, helping ensure your finances are working as effectively as possible.

Ongoing Reviews

Your plan shouldn’t stand still. Over time your income may change, your spending may evolve, markets will move and tax rules will shift. We update your forecast regularly so it continues to reflect your situation and keeps you on track.

A lot of people we speak to are in this exact position. This is a common situation for many people we speak to across Manchester who are approaching retirement and want clarity around their future finances.

They’ve built up pensions and savings, paid off the mortgage, and are now asking the question — can I actually afford to retire?

We recently worked with a couple in their late 50s with around £500,000 in pensions and savings, who had just paid off their mortgage and wanted to understand whether retirement was now possible.

After mapping out their spending, future plans and goals, we modelled their situation across hundreds of different market scenarios.

Initially, the plan showed a risk that their money may not last throughout retirement, particularly if markets performed poorly in the early years.

Rather than this being a yes or no answer, it allowed us to explore options.

By adjusting their approach, including phasing into retirement by reducing working hours, we were able to significantly improve the sustainability of their plan while still aligning with what they actually wanted from retirement.

If you’d like to see how this works in practice, I’ve gone through this example in more detail here on this video.

Here’s what one client said after going through this process:

“After seeking help regarding management of my pension and savings, Matt provided me with some great advice and information which has had a big impact. Previously I did not have a long-term view of my personal finances and investments, and I didn’t appreciate the degree to which your actions now can affect your future finances & lifestyle.

Getting a long-term holistic view from Matt opened my eyes to this type of thinking and planning, and has given me a completely new perspective in terms of how to invest going forward. Further, Matt didn’t take a one size fits all approach and was keen to understand my goals as an individual and then provide me with the appropriate advice.

I would highly recommend Matt to provide sound and solid financial advice, backed by research and a keenness to do best by the individual and help them achieve their goals.”

Who This Service Is For

This is particularly useful if you:

What You’ll Get From Us

If you want to understand whether you’re on track and what your future could look like financially, we can build this out for you.

There isn’t a single number that works for everyone.

The amount you need depends on your lifestyle, retirement age and existing assets. For example, someone planning a more modest lifestyle may need significantly less than someone who wants to travel regularly or support family financially.

Cashflow modelling helps answer this properly by showing how your income, assets and spending interact over time, giving you a personalised view rather than relying on general rules of thumb.

Understanding what income you might need in retirement can be difficult, but there are a couple of useful starting points.

As of April 2026, the Retirement Living Standards suggest that for a moderate lifestyle, a single person may need around £31,700 per year, while a couple may need around £43,900 per year. This typically covers essentials, some discretionary spending and a couple of holidays each year. Please note these are current figures and are updated regularly to reflect changes in inflation, so for the latest amounts, it’s worth checking the Retirement Living Standards website.

Another approach is the replacement rate method, which looks at replacing a percentage of your current income. For example, someone earning between £31,500 and £45,000 may aim to replace around 67% of their income in retirement.

These are useful guidelines, but they don’t take into account your personal circumstances. That’s why we use cashflow modelling alongside a detailed breakdown of your spending, so you can build a plan based on what you actually need.

Cashflow modelling isn’t about predicting the future perfectly. It’s about giving you a realistic guide based on your current position.

By testing your plan across a wide range of historical scenarios, it shows how robust your plan is and where adjustments may be needed.

Yes, this is one of its main uses.

It allows you to see when your finances become sustainable and how different decisions, such as retiring earlier or reducing working hours, affect your long-term position.