Pension consolidation in Manchester can help simplify your retirement planning, especially if you’ve built up multiple pensions across different jobs. This can make it harder to understand the bigger picture. Are they invested in the right way? Should I consolidate these pensions? How should I draw income from them when the time comes?

Many clients we work with across Manchester find they have pensions spread across multiple providers without a clear strategy.

Many people aren’t entirely sure what pensions they have, how they each work, how they’re invested, or how much they’re paying in charges.

Workplace pensions are often set up years ago and not reviewed. Over time, you might change jobs and end up with a collection of pensions spread across different providers, each with their own investment strategy, benefits, and way of operating.

These may include a mix of defined contribution pensions, where the value depends on contributions and investment performance, and defined benefit (final salary) schemes, which provide a promised level of income in retirement. Each type needs to be assessed carefully before any changes are made.

You may benefit from reviewing your pensions if you’re asking yourself:

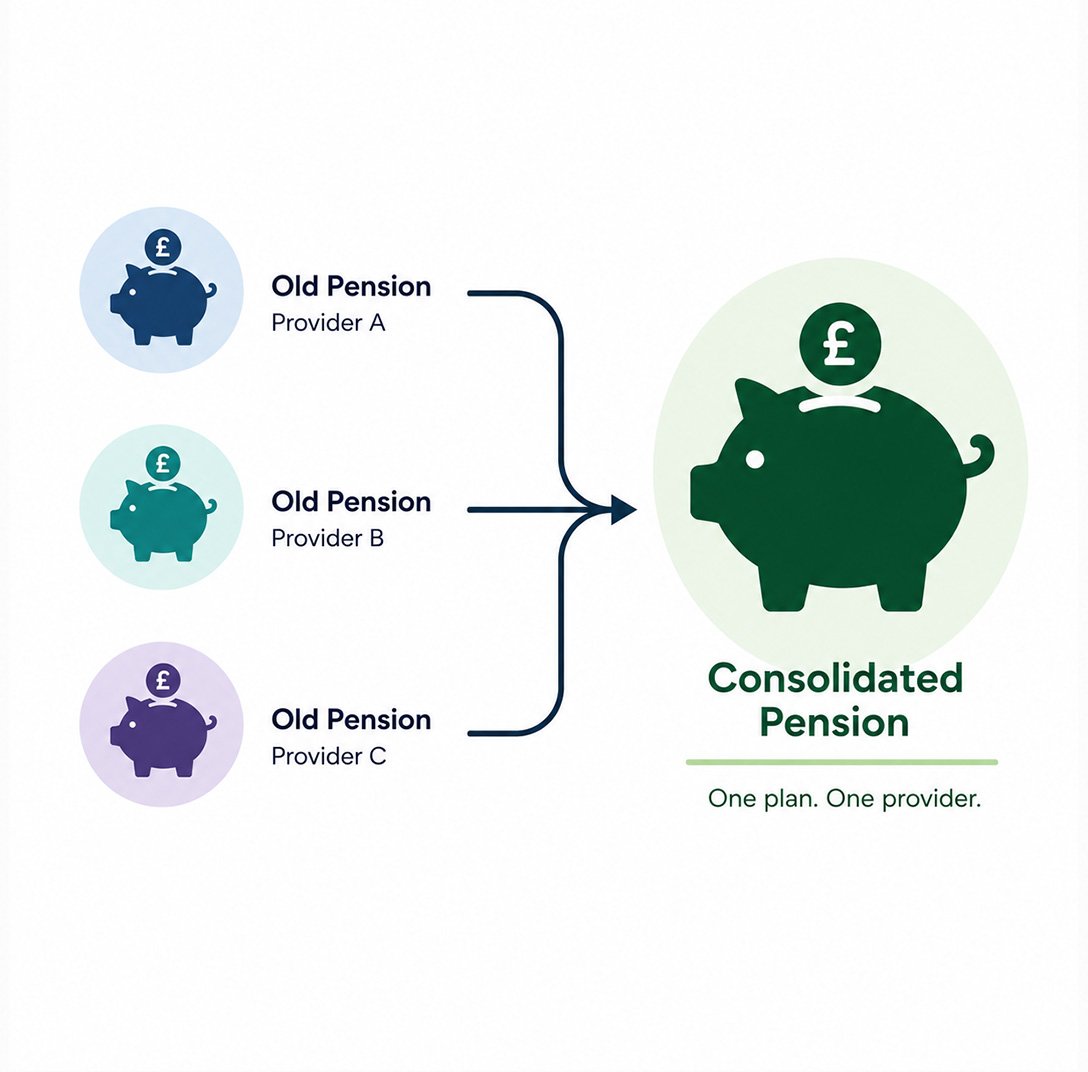

Consolidating pensions isn’t about transferring older ones into a new arrangement for the sake of it. It’s about making sure your retirement savings are working as efficiently as possible.

When appropriate, consolidation can:

However, consolidation is not always the right decision. Some older pensions may contain valuable guarantees, protected tax-free cash, or safeguarded benefits. Before recommending any transfer, we carefully assess whether moving the pension is suitable — and if it isn’t, we explain why.

The first step is getting a full picture. We gather information from your providers to understand:

Only once we understand what you already have can we decide whether change is appropriate.

We then assess whether consolidating pensions would improve your overall position. Sometimes bringing your pensions together can create simplicity and cost efficiency. Other times, keeping them separate may preserve valuable benefits you don’t want to lose. Every recommendation is based on your specific circumstances.

At some point, your pensions will need to provide income. There are different ways you can do this, including:

The right approach depends on your circumstances, retirement plans, tax position and need for flexibility. For example, someone retiring gradually may benefit from phased withdrawals, whereas someone who prefers certainty may benefit from purchasing an annuity.

We also consider how pension withdrawals interact with your personal allowance and other tax bands, alongside other assets such as ISAs and future income sources including the State Pension.

The aim is to withdraw income in a way that supports your lifestyle whilst managing tax efficiently.

Once we’ve agreed on the right structure for your pensions and income strategy, we take care of putting everything in place.

That may include arranging pension transfers, setting up new pension arrangements where appropriate, adjusting investments, or establishing a regular retirement income. We handle the paperwork, liaise with providers, and ensure each step is completed accurately and efficiently.

It depends. Consolidation can improve clarity and reduce complexity, but it is not automatically the right choice. Some pensions include valuable guarantees or benefits that should not be given up lightly. A full review helps determine whether consolidation genuinely improves your position.

There are a number of options when it comes to taking income from your pension when you reach pension access age, and the right choice depends on your circumstances and retirement plans.

One of the most common approaches is flexi-access drawdown or taking income using UFPLS (Uncrystallised Funds Pension Lump Sums). These options allow you to keep your pension invested and withdraw money as and when you need it. Typically, up to 25% can be taken tax-free, with the remaining withdrawals taxed as income.

The benefit of this approach is control. You can vary how much you take each year depending on your needs, and your pension remains invested with the potential for further growth. However, because the money stays invested, its value can rise and fall. Withdrawals need to be managed carefully to help ensure your pension lasts throughout retirement.

Another option is purchasing an annuity. Typically, with an annuity, you would take 25% of your pension as tax-free cash. The remaining funds are used to purchase an annuity, with the annuity provider agreeing to pay you a guaranteed income for life or for a fixed period.

The level of income you receive will depend on factors such as your age, health, annuity rates and whether you choose options such as inflation protection or benefits for a spouse.

Overall, drawdown is now more commonly used, as it allows greater flexibility around income and planning. However, annuities still have an important place for those who value guaranteed income and prefer not to be exposed to market fluctuations.

The right approach depends on your retirement goals, attitude to investment risk, health, tax position and wider financial circumstances. Retirement income planning isn’t just about choosing an option — it’s about creating a structure that supports your lifestyle both now and in the years ahead.

In most cases, yes — although not on all of it.

Under current UK rules, you can usually take up to 25% of your pension as tax-free cash. Any withdrawals beyond that are treated as income and taxed at your marginal rate in the year you take them.

This means the amount of tax you pay depends on your total income at the time — including salary, other income e.g. rental, the State Pension, or other pensions. Taking large withdrawals in a single tax year could push you into a higher tax band.

Careful planning can help manage this. By spreading withdrawals across tax years, using your personal allowance efficiently, and coordinating pension income with other assets such as ISAs, it’s often possible to reduce unnecessary tax.