A case study using cashflow modelling — written in June 2026

Summary

Can you retire at 55 with a £300,000 pension? In this case study, we show how a 55-year-old with a £300,000 pension could potentially phase into retirement using a combination of State Pension income, an appropriate investment strategy, reduced working hours and flexible withdrawals.

Key Takeaways:

- A £300,000 pension is unlikely to support a £26,400 annual income from age 55 without additional planning

- State Pension income can significantly improve retirement sustainability

- Phased retirement can have a bigger impact than many people realise

- Spending flexibility can dramatically reduce the risk of running out of money.

- Cashflow modelling helps test different retirement strategies before making decisions.

Is £300,000 enough to retire at 55?

One of the most common questions I get from people approaching retirement is some version of: “I’ve got X amount in my pension — is that enough to stop working?”

The honest answer is: it depends. It depends on some very specific things — how much income you need, when the State Pension kicks in, how you invest your pot, and how flexible you can be if markets fall more than expected early in retirement.

In this blog, I’m going to walk through a real-world case study using cashflow modelling software to show you exactly what the numbers look like — and what levers you can pull to make a £300,000 pension go further.

Meet Alex

Alex is 55 years old. He’s single, has £300,000 in his pension, and he wants to know whether he can retire right now. He has no mortgage and no other significant assets.

Step 1: Work Out the Income Need

Before we look at the pension, we need to understand what retirement actually needs to cost.

Alex has worked through his expenses by looking at his essential costs and discretionary costs. He estimates he needs £2,200 per month after tax in retirement so an annual amount of £26,400

Step 2: How Can Alex Take Income From His Pension?

There are two broad approaches — flexible income (drawdown) and fixed income (annuity). Let’s look at both briefly.

Option A: Drawdown

With drawdown, Alex keeps his pension invested and takes withdrawals as needed. He can take more in some years and less in others. The pot remains his, and unused funds can be passed on. The risk is that if markets fall badly — particularly early in retirement — the pot can deplete faster than expected.

Option B: Annuity

An annuity converts your pension pot into a guaranteed income for life, provided by an insurance company. There’s no investment risk, but you lose flexibility and access to the capital.

With a £300,000 pension, Alex would typically take his 25% tax-free cash first (£75,000), leaving £225,000 to purchase an annuity.

Based on annuity quotes obtained on 18 June 2026, a £225,000 annuity could provide a guaranteed income of approximately:

- £15,632 per year if taken on a fixed level basis, where the income remains the same throughout retirement and does not increase with inflation; or

- £9,520 per year if taken on an RPI-linked basis, where the income increases each year in line with the Retail Prices Index (RPI), a measure of inflation.

These figures are for illustration only and are based on annuity rates available at the time of writing. Annuity rates change regularly and the income available will depend on factors including age, health, options selected, and market conditions at the point of purchase.

The key point is that an annuity can provide certainty and peace of mind, but that security comes at a cost. The inflation-linked option starts at a much lower income level, while the level annuity risks losing purchasing power over time as prices rise.

And crucially, at age 55, you’re potentially buying an income that may need to last for 40 years or more. That’s a significant commitment, and once an annuity has been purchased, the decision is generally irreversible.

In Alex’s case, he wants flexibility, so let’s focus on the drawdown route — and that’s where cashflow modelling plays a key role.

Step 3: What Does the Cashflow Modelling Show?

I use cashflow planning software provided to stress-test retirement plans. The software uses over 100 years of real historical and inflation market data to model what happens to a plan across hundreds of different economic scenarios.

For this plan, I’ve modelled Alex drawing £26,400 per year in today’s money (inflation-adjusted), with a 60/40 equity/bond portfolio and total costs of 1% per annum. We’re running scenarios to age 97.

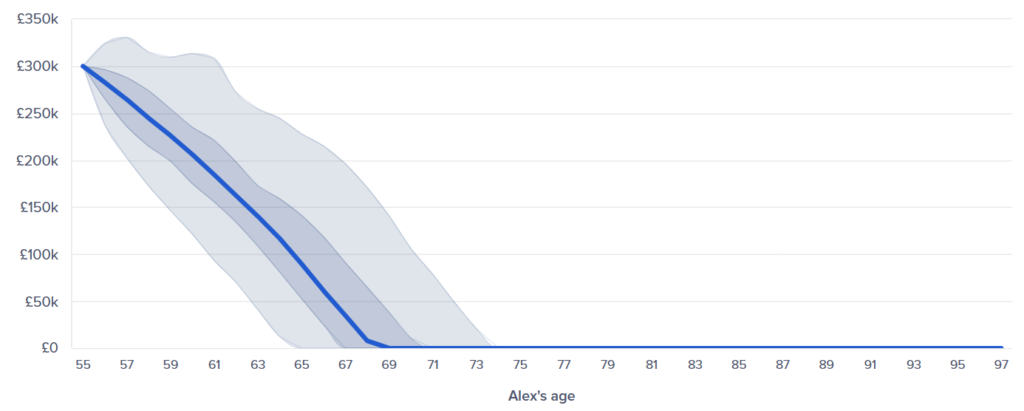

Starting Point: No Changes

Based on 780+ scenarios drawn from over a century of market history, Alex’s pension runs out of money in every single scenario before he reaches 97.

Success rate: 0%.

That doesn’t mean it’s impossible to retire at 55 with £300,000. However it means we need to look at what we can change.

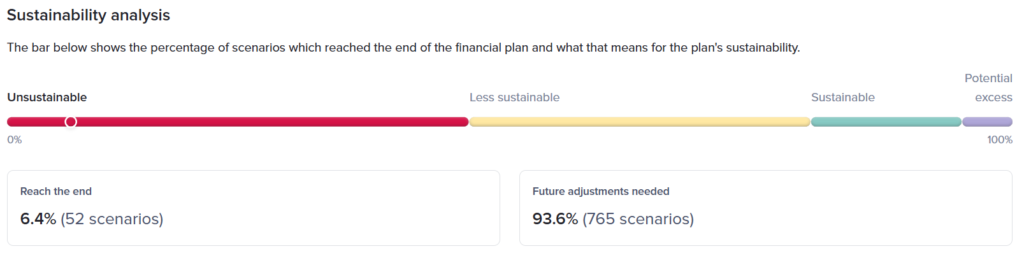

Lever 1: Add the State Pension

Alex is currently 55 and is expected to qualify for the State Pension at age 67, which is 12 years away.

The full new State Pension in 2026/27 is £241.30 per week — that’s £12,548 per year which we’ll assume is inflation adjusted by the time he reaches state pension age. Once it starts, Alex needs a net withdrawal of £13,852 per year from his pension to maintain his lifestyle.

Reducing withdrawals by almost half has a meaningful impact on the sustainability of the plan, but it doesn’t solve the problem entirely.

Below is our sustainability analysis:

Better. But 6% is nowhere near good enough to hang retirement plans on. Let’s see what else we can do.

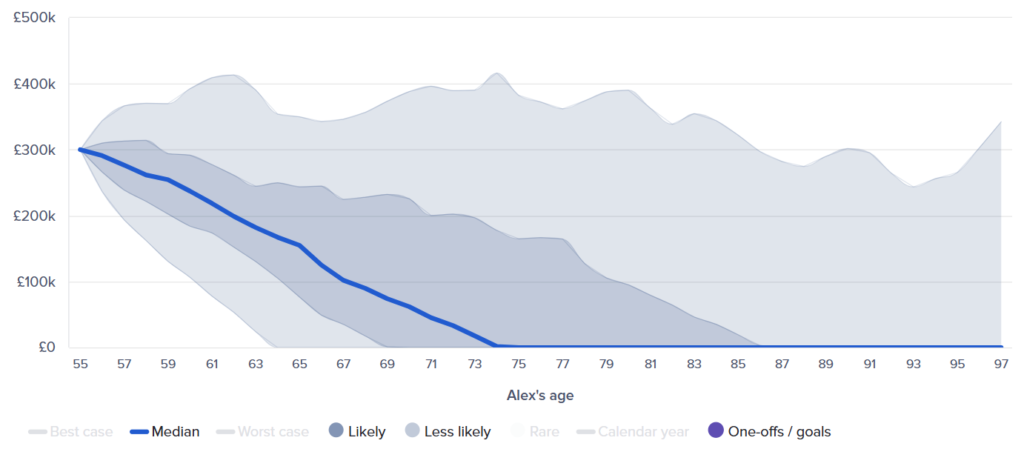

Lever 2: Increase Equity Allocation

Alex’s pension is currently invested in a portfolio made up of 60% equities and 40% bonds. One option we explored was increasing the level of investment risk by moving the portfolio to 100% equities, while also holding one year’s worth of planned withdrawals in cash within the pension.

The chart below shows the range of outcomes after making this change.

Equities have historically delivered higher long-term returns than bonds, although they tend to have greater short-term volatility. Holding a cash reserve alongside the portfolio provides a useful buffer. If markets fall, Alex can draw his income from the cash pot rather than selling investments when their value is temporarily lower.

Combining a higher equity allocation with a one-year cash buffer improves the outlook. The probability of success increases to 20%, and the median outcome now sees the pension lasting until age 74.

It’s an improvement, but it still falls well short of funding a retirement that could last 30 or 40 years.

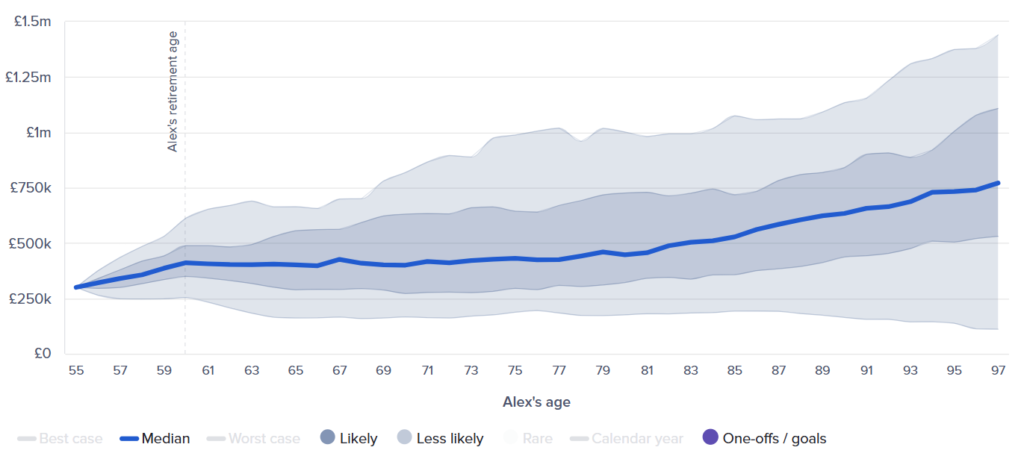

Lever 3: Phase Retirement Rather Than Fall off a Cliff

Retirement doesn’t have to be an all-or-nothing decision, and that flexibility is what was needed to make a significant difference for Alex.

Most people think of retirement as a cliff edge: you’re working full-time on Friday, and on Monday you’re fully retired. But there’s a middle ground — phased or semi-retirement.

Alex currently earns £60,000. If he drops to three days a week for the next five years until age 60, his income falls to roughly £36,000 gross — which covers his lifestyle costs without touching the pension. During those five years:

- The pension pot isn’t being drawn down

- Investment growth has more time to compound

- Alex and his employer continue contributing to the pension

- Alex has time to adapt to retirement before stopping work completely

After five years of phased retirement, the modelling shows Alex’s pension pot grows to approximately £411,000 at age 60 and his sustainability score is 70%. Now we’re in genuinely comfortable territory. Most scenarios end with money still in the pot at 97.

However, that also means there is around a 30% chance that the pension runs out before age 97. At first glance, that might sound concerning. But age 97 is a long way into the future, so the next question we need to ask is: what are the chances that Alex is still alive at that point?

Longevity-Adjusted Planning

This is where longevity-adjusted planning becomes useful. Rather than simply asking whether the pension lasts to a particular age, we can look at the probability of Alex both running out of money and still being alive to experience the shortfall.

As you can see, the probability of running out of money increases as Alex gets older. However, the probability of being alive also falls over time. By combining these two factors, we can calculate a longevity-adjusted risk — the chance that Alex has exhausted his pension while still needing it.

The period of greatest risk sits roughly between ages 81 and 88, where the probability of Alex running out of money while still being alive peaks at around 13–14%.

For many people, that level of risk may be acceptable, particularly given the flexibility and spending power available throughout retirement. But if Alex wants even greater certainty, there is one final lever we can pull.

Lever 4: Build in Spending Flexibility (Boundaries)

Even after introducing phased retirement, there remains a risk that Alex could run out of money later in life if investment returns are particularly poor.

Retirement plans often become unsustainable because poor market returns occur early in retirement while withdrawals continue unchanged. This is known as sequence of returns risk.

One way to manage this risk is to agree in advance how spending will be adjusted if things don’t go to plan. Rather than making emotional decisions during a market downturn, we can use a rules-based approach known as boundaries.

How Boundaries Work

Each year, we look at Alex’s pension withdrawal as a percentage of the pot’s current value.

If the pot has fallen significantly (say, after a market crash), the withdrawal rate as a percentage will have risen. If it rises above a set threshold, Alex reduces his spending to protect the pot.

If the pot has grown strongly, the withdrawal rate will have fallen. If it drops below a lower threshold, Alex can spend a bit more — the plan is ahead of schedule.

| Alex’s Boundaries

Target: £26,400 net per year For the first 15 years of retirement:

|

This kind of systematic flexibility — knowing in advance what you’ll do if things go wrong, rather than making emotional decisions during a crash — is one of the most powerful tools in retirement planning.

Importantly, we’re not talking about dramatic lifestyle changes. A 10% adjustment is designed to be manageable while still having a meaningful impact on the long-term sustainability of the plan.

The impact is significant. By building a small amount of flexibility into the plan, the likelihood of Alex’s pension lasting to age 97 rises to 93%. More importantly, the chance of Alex both running out of money and still being alive falls to less than 1% at every age up to 98.

Conclusion: Is £300,000 Enough to Retire at 55?

For many people, yes. For others, no. But probably not in the way most people think.

When we first modelled Alex’s retirement, the outlook wasn’t particularly encouraging. The pension simply wasn’t large enough to support his desired lifestyle for the rest of his life without making some changes.

Many people focus on the size of their pension pot, but retirement planning is about much more than that.

The real question is: in your retirement plan what matters the most to you?

The Four Levers That Improved Alex’s Plan

By making a series of sensible adjustments, Alex’s retirement became significantly more sustainable:

- Factoring in his future State Pension.

- Reviewing how his pension was invested.

- Phasing into retirement rather than stopping work immediately.

- Building flexibility into his withdrawals through a boundaries approach.

None of these changes were dramatic on their own, but together they transformed the outcome. For Alex, the difference between failure and success was making a series of sensible adjustments that worked together.

Retirement planning isn’t about predicting the future. It’s about understanding the risks, identifying your options and building a plan that can adapt as life unfolds.

For Alex, £300,000 wasn’t enough to retire at 55 without compromise. But with the right strategy and a willingness to remain flexible, retirement became a realistic and achievable goal.

Want to Know If Your Retirement Plan Is On Track?

Every situation is different. The numbers here are illustrative — they’re designed to show you some of the factors that matter and the decisions you’ll face, not to tell you what to do.

Alex’s situation is only one example. If you’re married, have other savings, expect an inheritance, have defined benefit pensions or want a different level of retirement spending, the results will be different.

If you’d like to run your own numbers with a personalised cashflow model and a review of your retirement plan — one that accounts for your specific pensions, State Pension entitlement, tax position and income goals — please get in touch using the ‘Talk To Matt’ button.

Frequently Asked Questions

Is £300,000 enough to retire at 55?

In many scenarios, yes — but not without some planning. As the case study shows, neither taking an inflation-linked annuity nor immediately entering drawdown was sufficient to sustainably support Alex’s desired level of spending. However, combined with a phased retirement, an appropriate investment strategy and some spending flexibility, it can work.

Is drawdown or an annuity better for me?

Neither is universally better. Annuities provide certainty and protection against longevity risk. Drawdown provides flexibility and the potential for growth but requires more ongoing management. If you get in touch, we can help you decide what options makes sense for your circumstances.

What is the minimum pension age?

Currently 55. This is rising to 57 from 6 April 2028. If you’re affected by the increase, check whether your pension scheme offers a protected pension age which may allow you to access benefits before age 57.